Many employees view Incentive Stock Options (ISOs) as a golden ticket to wealth, especially when a company is on the verge of an Initial Public Offering (IPO). However, the reality of pre-IPO investment is often far more complex, involving a “liquidity trap” that can lead to devastating financial consequences. When an investor exercises ISOs in a private company, the “bargain element”—the difference between the strike price and the fair market value—triggers the Alternative Minimum Tax (AMT). Because private shares cannot be sold on an open exchange, investors often find themselves facing a massive, out-of-pocket tax bill for an asset they cannot liquidate. This risk is further compounded by unpredictable IPO timelines, underwriter lock-up periods, and trading blackouts that can keep shares out of reach for years, even after a company successfully goes public.

If you or a loved one suffered significant losses due to a broker’s failure to disclose the risks of a fraudulent pre-IPO investment, the team at Meyer Wilson Werning is ready to help. We investigate whether your advisor met their legal duties — and whether your losses are the result of actionable misconduct. Contact us today for a free and confidential consultation — you pay nothing unless we recover for you.

How Pre-IPO Incentive Stock Options Can Lead to Significant Losses

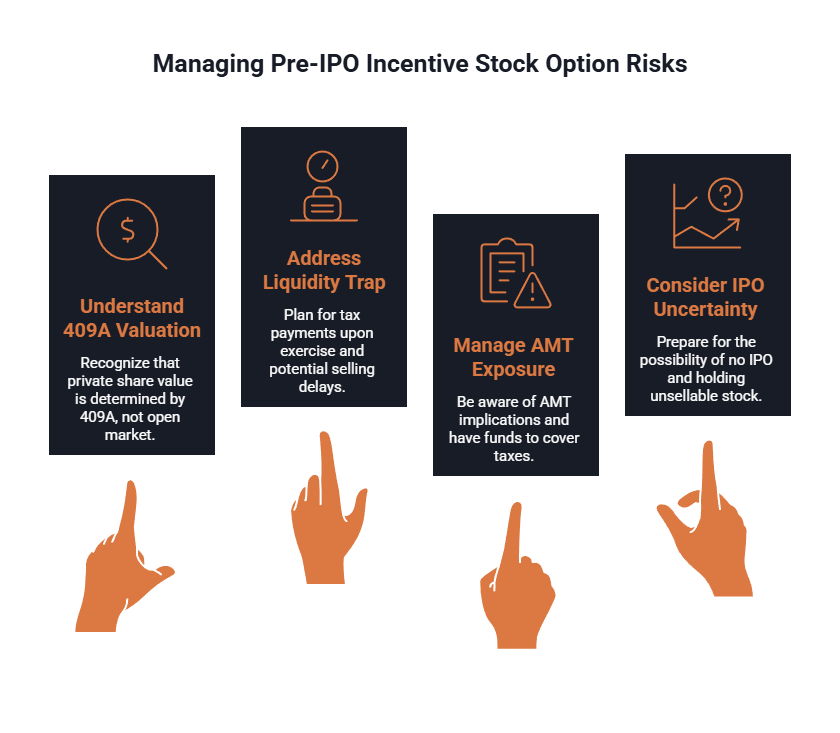

ISOs give employees the right to purchase company shares at a fixed strike price. However, unlike public stocks, the “fair market value” of private shares is determined by a 409A valuation, not an open market price. This lack of transparency is where many broker negligence claims begin.

Important Points Regarding ISO Risks:

- The Liquidity Trap: You may be required to pay taxes immediately upon exercise, but company plan rules or transfer limits can prevent you from selling shares for months or even years.

- AMT Exposure: The “bargain element”—the difference between your strike price and the fair value—counts toward AMT. If you cannot sell shares to cover the tax, you must pay it out-of-pocket.

- IPO Uncertainty: There is no guarantee a company will ever go public. If the IPO stalls or never happens, you could be left holding unsellable stock of little value after paying a high tax bill.

We Have Recovered Over

$350 Million for Our Clients Nationwide.

How IPO Delays, Lockups, and AMT Drive Risk

Even when a company is successful, the road to liquidity is often blocked by corporate hurdles. An advisor who fails to model these windows may be providing unsuitable advice.

Common Barriers to Selling Shares:

- Underwriter Lock-ups: Most companies prohibit employees and insiders from selling shares for six months following an IPO.

- Trading Blackouts: Internal rules often block sales for the two months preceding an earnings report, leaving only small “open windows” for trading.

- Qualifying Dispositions: To receive favorable tax rates, you must meet specific holding periods, which further delays your ability to exit the position.

The math shows how quickly these risks escalate. Exercising 10,000 shares at a $1 strike when the value is $2 creates a $2,800 tax bill at the 28% AMT rate. If you wait two years until the price hits $35 post-IPO, that tax bill jumps to $95,200. Without a clear liquidity plan, these tax liabilities can bankrupt an unprepared investor.

Red Flags of Negligent Recommendations and Misconduct

Financial advisors have a legal duty under FINRA Rule 2111 (Suitability) and FINRA Rule 3110 (Supervision) to protect their clients. Red flags that often lead to an arbitration claim include:

- Overconcentration: When an advisor suggests putting a large portion of your net worth into a single pre-IPO issuer.

- “Selling Away“: When a broker offers “ground floor” private placements that are not officially approved by their brokerage firm.

- Lack of Disclosure: Failing to explain the impact of AMT or the reality of IPO lock-up periods.

Our lawyers are nationwide leaders in investment fraud cases.

Seeking Recovery Through Arbitration

Investors who have been harmed by a pre-IPO investment scam or negligent advice have the right to seek recovery. This is typically done through arbitration, a structured process where a neutral panel reviews the evidence and issues a binding decision.

To build a strong case, we look for:

- ISO Grant Agreements and 409A valuations provided at the time of exercise.

- Tax records documenting the AMT paid and the resulting financial strain.

- Advisor communications where risks were minimized or IPO timelines were misrepresented.

We Are The firm other lawyers

call for support.

Investigation Update: NextGenTech and Sestante Capital

Our firm is currently monitoring the fallout from the NextGenTech Investments scheme. In December 2025, manager Giovanni Pennetta was charged with securities fraud for allegedly faking access to Anduril Industries shares and misappropriating investor capital.

While criminal charges address the fraudster, they do not always guarantee the return of lost funds. If your financial advisor recommended NextGenTech or Sestante Capital as a “safe” pre-IPO play, they may have failed in their due diligence obligations. Reach out if you held positions in this fund.

How Meyer Wilson Werning Supports Defrauded Investors

Navigating the complexities of Incentive Stock Options and pre-IPO investment losses requires more than just tax knowledge; it requires an understanding of the legal duties brokers owe their clients. If an advisor’s failure to explain AMT risks or lock-up restrictions has left you in a financial crisis, pursuing a claim for broker negligence through arbitration may be your best path toward recovery. Holding firms accountable for unsuitable advice is a vital step in seeking justice and recovering what was lost due to a lack of transparency and proper disclosure.

With more than 20 years in the industry and over $350 million recovered for clients, the attorneys at Meyer Wilson Werning have the experience and resources to hold negligent firms accountable. If you are facing an impossible tax bill or have lost money in a private equity deal, contact us today for a free and confidential consultation to discuss your recovery options.

Frequently Asked Questions

What is the “bargain element” in an ISO exercise?

The bargain element is the difference between the strike price you pay and the fair market value of the shares at the time of exercise. This “profit” is what triggers the AMT liability.

Why is AMT so dangerous for pre-IPO investors?

Because you cannot sell private shares on an exchange, you cannot use the proceeds of the sale to pay the tax. You must find the cash elsewhere, often resulting in a liquidity crisis.

Can I recover money from a broker for pre-IPO losses?

Yes. If your broker provided unsuitable recommendations or failed to disclose material risks, you may be able to recover money from the broker through an arbitration claim.

What is “selling away” in a pre-IPO context?

This occurs when a broker sells you a private investment that is not on their firm’s approved list. This is a major red flag and a violation of FINRA rules.

How long do I have to file a claim?

Time limits apply to all arbitration claims. It is critical to consult with an investment fraud attorney as soon as you suspect misconduct to ensure your rights are protected.

Recovering Losses Caused by Investment Misconduct.