According to a February 5, 2026, announcement by the U.S. Securities and Exchange Commission (SEC), more than $4.1 million is at issue in a case involving Marat Likhtenstein and the alleged misuse of self-issued promissory agreements. The SEC claims that while Likhtenstein was associated with Osaic Wealth, Inc., he diverted investor funds for personal use and Ponzi-like payments. Public filings state that a consent judgment is in place under Litigation Release No. 26476, with monetary relief to be determined at a later date. Furthermore, a parallel criminal action was reportedly announced by the Kings County District Attorney’s Office on March 12, 2025.

If you or a family member suffered losses tied to promissory agreements connected to Marat Likhtenstein or Osaic Wealth, the broker misconduct attorneys at Meyer Wilson Werning are reviewing investor claims now. Contact us today for a free and confidential consultation, and you pay nothing unless we recover for you.

What Sparked the Likhtenstein Case and Where It Stands Now?

The SEC’s complaint alleges a multi-year scheme running from April 2017 through June 2024. During this time, Marat Likhtenstein allegedly acted as an investment adviser to solicit and sell self-issued promissory agreements to at least 15 advisory clients. Instead of placing client funds in legitimate third-party investments, the SEC alleges the funds were misappropriated.

The civil action, filed in the Eastern District of New York on September 26, 2025, resulted in a consent judgment on February 4, 2026. This order includes injunctive relief to stop the alleged conduct, though the final dollar amount for restitution and penalties remains pending.

A Pattern of Regulatory Problems and Non-Cooperation

Beyond the SEC charges, Likhtenstein (CRD#: 2470480) has faced severe disciplinary action from the Financial Industry Regulatory Authority (FINRA):

- August 13, 2024: Likhtenstein submitted a Letter of Acceptance, Waiver, and Consent (AWC) to resolve allegations that he refused to provide information and testimony requested under FINRA Rule 8210.

- September 12, 2024: FINRA officially barred Likhtenstein from the securities industry following his failure to cooperate with an investigation into undisclosed personal loan transactions with a client.

- Osaic Wealth, Inc. (also referenced historically as Royal Alliance) was his most recent firm of record until June 2024.

We Have Recovered Over

$350 Million for Our Clients Nationwide.

What Were the Risks and Red Flags Associated with Marat Likhtenstein’s Promissory Agreements?

Promissory agreements are essentially IOUs, but when issued privately by an advisor rather than through an established financial institution, they often mask fraudulent activity. In the case of Marat Likhtenstein, public records and the SEC complaint highlight several important points that serve as critical warning signs. First, the agreements were self-issued by Likhtenstein himself rather than a transparent third party, which eliminated necessary independent oversight.

Furthermore, investors were allegedly given vague descriptions of how their money would be used, and pitch materials often promised high or “secure” returns that lacked any independent verification. Most significantly, the SEC alleges the scheme functioned as a Ponzi-like structure, where approximately $940,000 was used for circular payments to earlier investors to maintain an illusion of success, while $3.2 million was diverted to fund Likhtenstein’s personal expenses.

How Can Investors Pursue Recovery from Osaic Wealth Through Arbitration?

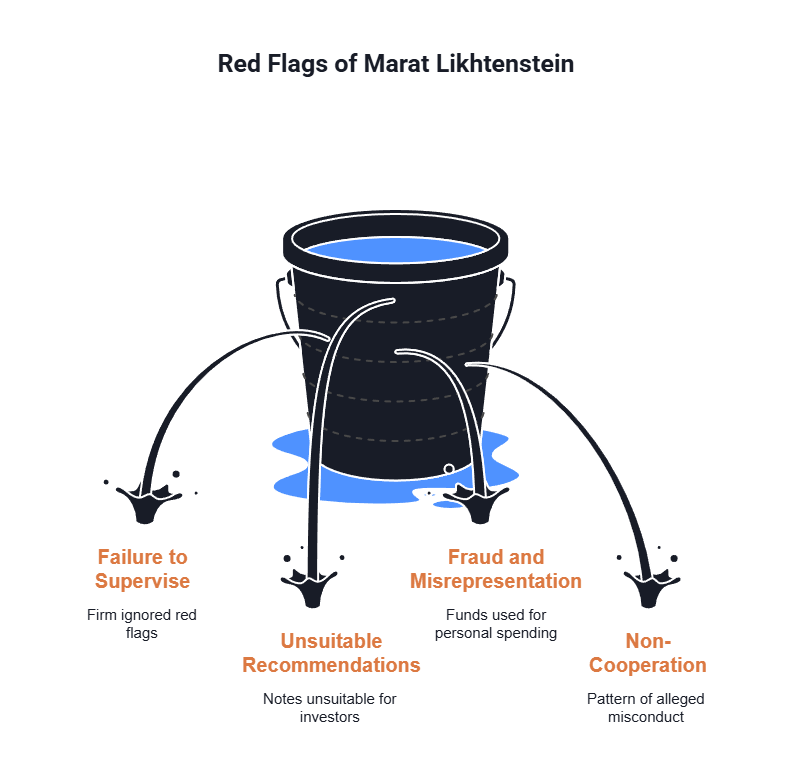

When a broker engages in “selling away”—selling investments not approved by their firm—the brokerage firm still has a legal duty to supervise that broker’s activities. Investors who lost money with Marat Likhtenstein may be able to pursue recovery through arbitration based on several key allegations:

- Failure to Supervise (Rule 3110): Osaic Wealth, Inc. was required to detect and prevent “selling away.” If the firm ignored red flags, it may be liable for the $4.1 million in losses.

- Unsuitable Recommendations (Rule 2111): Private, illiquid promissory notes are often unsuitable for retirees and conservative investors who require transparency and liquidity.

- Fraud and Misrepresentation: The SEC alleges $3.2 million funded personal spending while $940,000 went to Ponzi-like payments to sustain the scheme.

- Non-Cooperation (Rule 8210): The September 12, 2024, FINRA bar reinforces a pattern of alleged misconduct that firms should have identified.

Our lawyers are nationwide leaders in investment fraud cases.

How Meyer Wilson Werning Supports Defrauded Investors

The SEC alleges that $3.2 million went to Likhtenstein’s personal expenses and $940,000 was used to make circular payments to earlier investors. He was barred by FINRA for refusing to cooperate with investigators. Osaic Wealth had a legal duty to supervise his activities and detect the red flags of selling away. For the investors who trusted him with their savings, that oversight failure matters as much as the fraud itself.

For over 25 years, Meyer Wilson Werning has recovered more than $350 million for investors harmed by broker misconduct and supervisory failures. If you lost money through Marat Likhtenstein’s promissory agreements, contact us today for a free and confidential consultation. You pay nothing unless we recover for you.

We Are The firm other lawyers

call for support.

Frequently Asked Questions

What is the current status of the Marat Likhtenstein SEC case?

As of February 4, 2026, a consent judgment has been entered in the Eastern District of New York. While this order stops certain conduct, the court has yet to determine the final amount of monetary relief Likhtenstein must pay.

Why was Marat Likhtenstein barred by FINRA?

FINRA barred Likhtenstein on September 12, 2024, because he failed to cooperate with an investigation into potential undisclosed loans and other private activities while associated with Osaic Wealth, Inc.

Can I recover money if the investment was not on my official Osaic statements?

Yes. This practice is known as “selling away.” Under industry rules, firms are responsible for supervising the private securities activities of their brokers. If supervision fell short, the firm may be liable for investor losses in arbitration.

How do self-issued agreements create conflicts?

When an adviser issues their own agreements, they control the terms and the cash flows. This structure removes the independent oversight typically provided by third-party investment products and significantly increases the risk of fund misuse.

What documentation should I gather to pursue compensation?

Affected investors should collect all signed promissory agreements, wire confirmations, canceled checks, payment schedules, and any emails or pitch materials provided by the advisor. A clear timeline of what you were told is also vital for building a case.

Recovering Losses Caused by Investment Misconduct.